Atlanta: 2Q2021

Housing Market Analysis

Atlanta Housing Market Analysis

Atlanta’s strong recovery continued in 2Q21 despite growing concerns around affordability and the oncoming threat of the COVID-19 Delta variant. To-date, the Metro area has recaptured 78% of the jobs lost due to initial COVID-19 shutdowns and layoffs, and Atlanta currently boasts one of the country’s lowest Metro unemployment rates at just 3.6%. Atlanta’s housing market remains one of the brightest spots in the recovery as it continues to build on the momentum established in the second half of 2020 and the start of 2021.

The Atlanta housing market is currently being driven by the following factors:

Rapidly Declining Land Supply: VDL inventory has dropped by nearly -20% over the last 12 months, bringing the months’ supply down to just 19.3 months (lowest level since mid-2005). When you consider that as many as 25% of Atlanta’s VDLs are considered dormant (no activity in 2+ years), supply level drops to just over one year. Lack of supply is driving land prices upward, which is translating to higher home prices as builders struggle to preserve their profit margins. The lack of VDLs and suitable development sites continues to push new construction activity into secondary suburbs once considered too far from than the urban core to sustain large-scale residential development (5 of the top 10 selling communities are located 35+ miles from Downtown Atlanta).

High Construction Costs: The supply chain issues felt at the onset of pandemic in 2020 have not yet returned to “normal” levels with 80% of builders still reporting issues securing the materials and appliances necessary to complete new homes. The scarcity of these materials has driven their costs up, and it’s estimated that increased construction costs have added $32,000+ to the base cost of a new home in the current market. We’ve seen lumber prices edge down in recent weeks, however we have yet to see costs for other high-demand materials follow suit.

Increased Production: Despite both supply and pricing headwinds, builders ramped up lot development and new home construction through the first half of 2021 in an effort to meet the unprecedented levels of demand in the Atlanta market. Starts in 2Q21 reached their highest level since 2007 (although are still below the 2005 peak), and lot deliveries set new post-recession highs by reaching their highest level since 2008. As of the end of 2Q21, annualized housing starts and lot deliveries were up +29% and +15%, respectively, over the last 12 months.

Rising Home Prices: The aforementioned land scarcity and high construction costs, combined with a depleted housing inventory, have contributed to skyrocketing home prices across the Metro area. Resale home prices are up +22% YoY, and new single-family detached (SFD) and single-famly attached (SFA) home prices are up +11% and +22%, respectively, over the last 12 months.

Mortgage Rates

Source: Federal Reserve Bank of St. Louis

Source: Federal Reserve Bank of St. Louis

Although 30-year mortgage rates remained relatively steady through 2Q21, the gradual increase of rates since the record-low established in January has put pressure on buyers to purchase a home before rates creep up even further. While still at historically-low levels, mortgage rates have increased by 37 basis points since the start of the year.

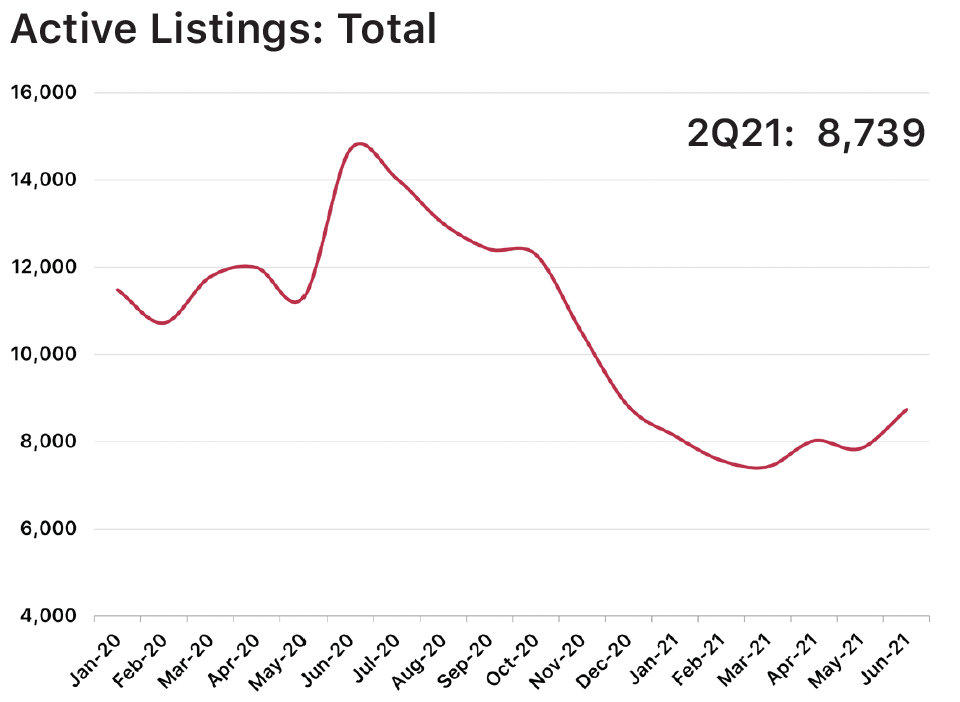

Active Listings

Source: Georgia Association of Realtors

Source: Georgia Association of Realtors

The total number of active home listings in Metro Atlanta increased by +17.6% from the end of 1Q21 as more owners listed their homes for sale in hopes of capitalizing on the significant price appreciation we’ve seen over the last 12 months. The months’ supply of active listings currently stands at just 1.3 months, a slight uptick from the 1.1 month supply at the end of 1Q21 but still drastically lower than what is considered “normal” for the Atlanta market (4-6 months). With increasing concerns around the COVID-19 Delta variant, we could see another pull-back of resale listings in 3Q21, which would further deplete the supply and push prices higher at an accelerated rate.

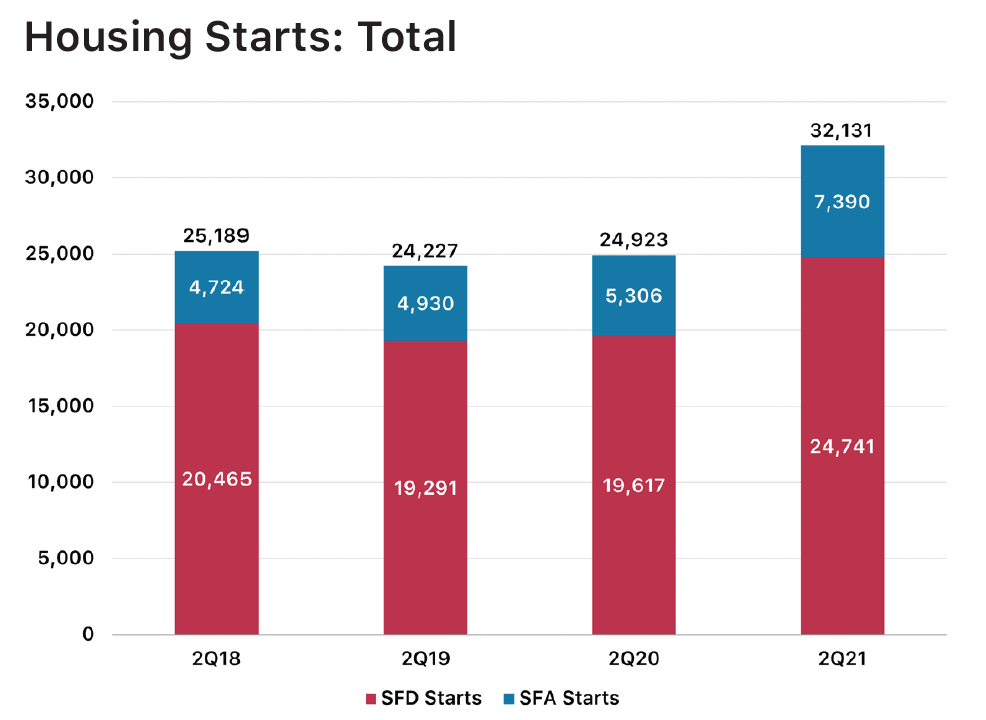

Housing Starts

Source: Metrostudy

Total annualized starts grew by +28.9% over the last 12 months, the largest year-over-year growth rate since 2Q14. SFD starts jumped +26.1% over the last 12 months, reaching their highest level since 4Q07. SFA starts jumped +39.3% since 2Q20 and are currently at their highest level since 4Q06. We expect both SFD and SFA starts to continue this upward trend based on the unprecedented level of demand, however elevated construction costs and a rapidly-dwindling VDL supply have the potential to cap the number of starts each builder can produce as we move through 2021.

Source: Metrostudy

Increasing land and materials costs continue to drive new home prices higher as builders increase their base costs to preserve their margins. While activity in the $200k-$250k range is fairly consistent with years past, there has been a dramatic uptick in starts for homes in the higher price tiers, most notably the $300k-$399k range. Starts in this price range jumped +62.3% since the end of 2Q20, and starts in the $400k-$450k range increase by +75.2% over the same period.

Home Closings

Source: Metrostudy

New home closings followed in line with starts, posting strong growth figures since the end of 2Q20. Total annualized closings are up +18.8% year-over-year and have reached their highest level since 4Q07. Annualized SFD and SFA closings increased by +14.5% and +36.2%, respectively, over the last 12 months - a trend we expect to continue through the end of the year as builders work through their backlog and fulfill pre-sale orders from late 2020 and the first part of 2021.

Lot Deliveries

Source: Metrostudy

The “if you build it, they will come” mentality appears to be in full force throughout the Metro area as the significant increase in starts in the upper price tiers translated directly to a significant increase in closings. Closings dropped in all price tiers below the $250k mark, but increased by +46.0% in the $300k-$399k range and +45.6% in the $400k-$499k range. We expect pricing to cool slightly through the end of 2021 as construction costs and resale inventory return to more reasonable levels.

Source: Metrostudy

Lot deliveries across Metro Atlanta increased by +14.6% since the end of 2Q20, adding a much-needed 20,400 lots to the market. Even this double-digit increase in lot production doesn’t fill the market’s supply-demand gap, however, as those 20,400 were immediately absorbed by builders. Atlanta needs to drastically increase lot development over the next 6-12 months to even scratch the surface of current demand for new housing.

Source: Metrostudy

Of the 202,329 future lots in Metro Atlanta, nearly 83% of them are considered to be dormant, indicating that while those lots have been planned for future development, there has been no development, construction, or sales activity in the last 2+ years. Based on the alarmingly low inventory of VDLs in this market, it is possible we will see more of these dormant lots come back online over the next 12-18 months.

Inventory & Supply

Source: Metrostudy

SFD VDL inventory declined by -19.0% since the end of 2Q20, and there are just over 42,300 VDLs in the market (a huge majority of which are already spoken for by builders). Decreasing inventory combined with a significant spike in sales has driven Atlanta’s VDL supply down to just 20.6 months (a -35.6% drop from the end of 2Q20).

Source: Metrostudy

SFA VDL inventory declined at almost the same rate as SFD inventory with overall inventory dropping by -19.0% over the last 12 months. The months’ supply for SFA VDLs dropped to just 15.0 months, a -39.8% decline from the end of 2Q20. We expect the supply of both SFD and SFA VDLs to decline so long as starts continue to drastically outpace deliveries.

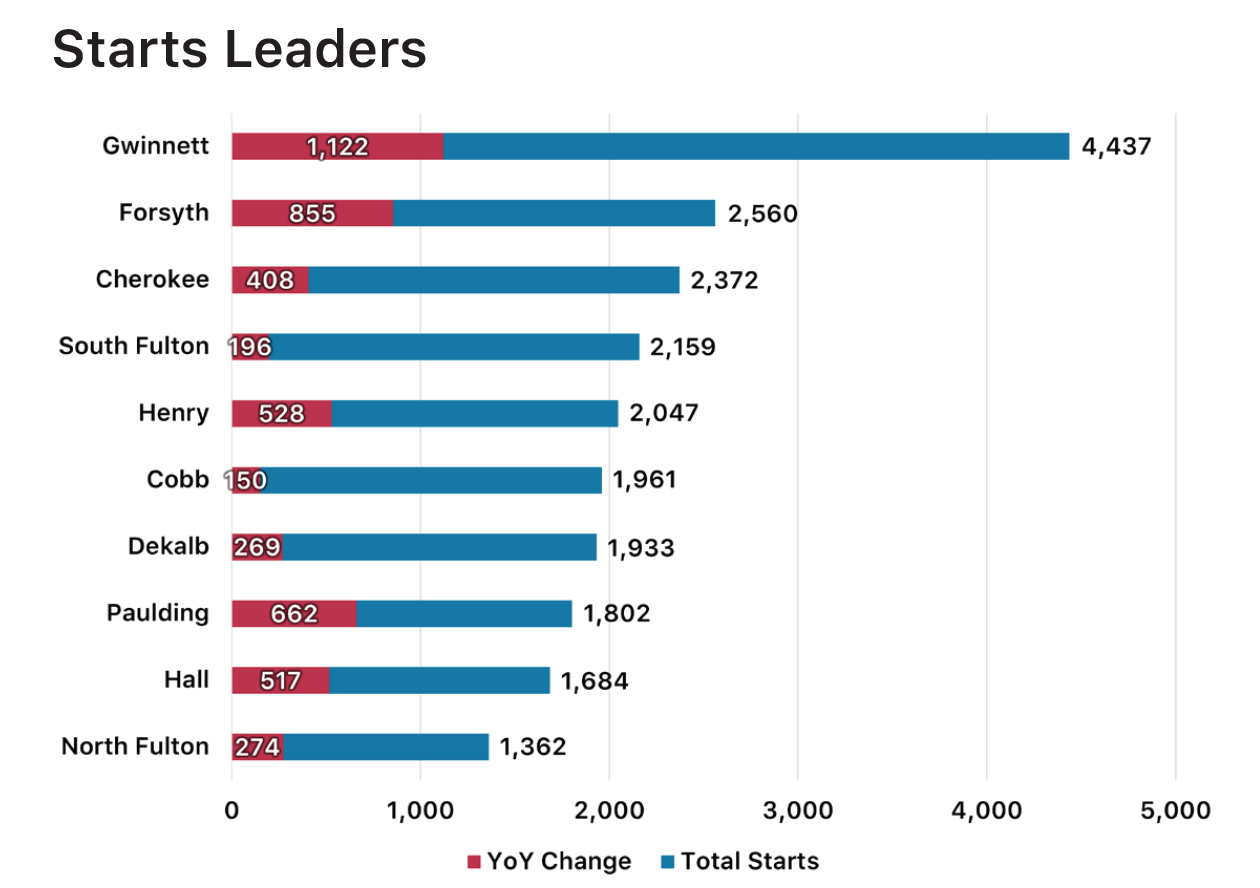

Market Leaders

Source: Metrostudy

Gwinnett County continues to lead the Metro area in housing starts with nearly 4,500 since the end of 2Q20, a +33.8% increase over the total number of starts in the previous 12 month period. Of the 23 counties comprising the Atlanta MSA, 21 of them experienced a double digit percentage increase in starts over this period. These figures reinforce the notion that home construction activity is increasing in all corners of the Metro Area instead of just the core “close-in” suburban counties of Cobb, Gwinnett, and Fulton as we’ve seen in the past.

Source: Metrostudy

Gwinnett tops the closings chart as well, thanks in large part to strong schools and excellent connectivity to the urban core. Closings in Gwinnett increased +31.7% over the last 12 months, making it one of 17 Atlanta counties that experienced double digit percentage growth in closings since the end of 2Q20. We anticipate that counties once considered secondary, such as Cherokee and Forsyth, will continue to account for an increasing number of home sales as land prices skyrocket and lot inventory dries up in closer-in counties like Gwinnett and Cobb.

Source: Metrostudy

15 of the Atlanta MSA’s 23 counties increased lot production since the end of 2Q20, led by Henry County’s +104.7% increase (+910 additional lots) and Cherokee County’s +69.0% increase (+812 additional lots). We expect that lot deliveries in heavily developed counties like Gwinnett, Cobb, and North Fulton to continue to dwindle due simply to the lack of suitable land for lot development in these counties. This will create gaps that those historically “secondary” counties like Cherokee, Henry, and Barrow are primed to fill just based on the sheer availability, and therefore more competitive pricing, of land in these submarkets.

Source: Metrostudy

The top performing submarket in the Metro Atlanta area over the last 12 months was South Fulton County, specifically in the sub-$250k price range. The $200k-$250k range has historically been the most popular amongst Atlanta residents, and it appears as that this trend will continue - at least until the lot inventory for sub-$250k homes completely dries up. Perhaps the most notable figure included above is the extremely low VDL supply in each of these top submarkets; 9 of the top 10 submarkets have less than a one-year supply of VDLs in their most popular price range.

Active Communities

Over the last several years, we’ve seen new home construction activity spread into Atlanta’s outer suburbs as land scarcity and pricing become increasing concerns in the counties that once dominated the market. The Work-From-Home movement that began at the onset of the pandemic has encouraged more and more families to seek larger homes in more private communities, even if those opportunities move them farther from the city center than they would have previously entertained.

Six of Atlanta’s top 10 performing new home communities are located more than 25 miles from the urban core, with five of those six being located more than 35 miles from the heart of Atlanta. The three communities closest to the urban core are hybrid, high-density communities offering attached housing or a mix of detached and attached.

Leading Builders

DR Horton continues to lead active homebuilders in Atlanta, selling nearly 900 homes in 2Q21 and eclipsing 3,600 in annualized sales - more than twice the number of closings by the second-ranked builder. Builders that already have a pipeline of VDLs or developable future lots will continue to dominate this market given the rapidly declining suppy of viable lots. The fact that three of the top five builders saw closings decrease from 1Q21 to 2Q21 is evidence of two major trends we are seeing in the Atlanta market: 1) builders are intentionally capping home sales due to overwhelming backlogs and increasing construction costs, and 2) lots are being consumed at a rate far greater than new ones are being delivered, and this will have an increasingly limiting effect on home construction and sales in the coming months.

Conclusion

After reviewing the data enclosed in this report, it’s easy to understand why there is so much optimism and excitement surrounding Atlanta’s housing market: developers and builders are ramping up lot deliveries and new home construction, resale inventory continues to grow as more sellers jump in the market to take advantage of record-high prices, and demographic trends continue to push more prospective buyers into the market.

As we progress into the second half of 2021, there are several factors that we should monitor closely as they could potentially have a negative impact on Atlanta’s housing market:

Resurgence of COVID-19 and Delta Variant Concerns: Employment, especially in the still-struggling Leisure & Hospitality sector, could be negatively impacted if COVID-19 infection rates continue to climb at the current pace and local and state governments are forced to reinstate restrictions on in-person dining, entertainment events, etc. In regards to the housing market, a continued resurgence of the virus could cause resellers to pull their listings due to fears of infection, causing the already-depleted resale inventory to shrink further.

Home Prices and Affordability: The two buying segments most impacted by increasing affordability concerns also happen to be the two largest buying segments: first-time and first-move up home buyers. Entry level home prices are up +19% YoY, which has priced thousands out of these buyers out of the market. Homes in the outer suburbs will continue to provide more affordable new home opportunities as compared to the closer-in suburbs, however we expect prices in all submarkets to continue their overall upward trajectory given the increasing scarcity of suitable development sites and the elevated costs of construction.

Extended Construction Times: While we are optimistic that lumber and other materials costs will continue their slow return to pre-pandemic levels, more than 80% of builders are still reporting pricing and supply chain issues. Builders will likely continue to intentionally slow the pace of home construction and closings while they combat pricing & lot inventory issues and work through their overwhelming backlogs.

The Return of Seasonality: Last year, seasonality all but disappeared in the Atlanta market. In 2020, home construction and sales ramped up in the summer months and continue to climb through the fall and winter due to pent-up demand and sub-3% mortgage rates. This year, however, we see sales figures have followed more traditional patterns of ramping up in the summer months and cooling off as we enter the fall.

As we enter 3Q21, year-over-year comparison figures will start painting a very negative picture of where the housing market is. It is important to keep in mind that any talk of a “slow-down” in the housing market is relative to the record-high sales and starts numbers we saw in the second half of 2020 and almost all housing metrics remain well above long-term average levels. It is also important to remember that any declines in starts and sales we see in the coming months will not be a result of waning demand, rather a lack of suitable lots for homebuilding and the intentional throttling of sales by builders.

For information about market research & reporting, including custom market reports, please contact Katie Fidler at katief@stbourke.com.